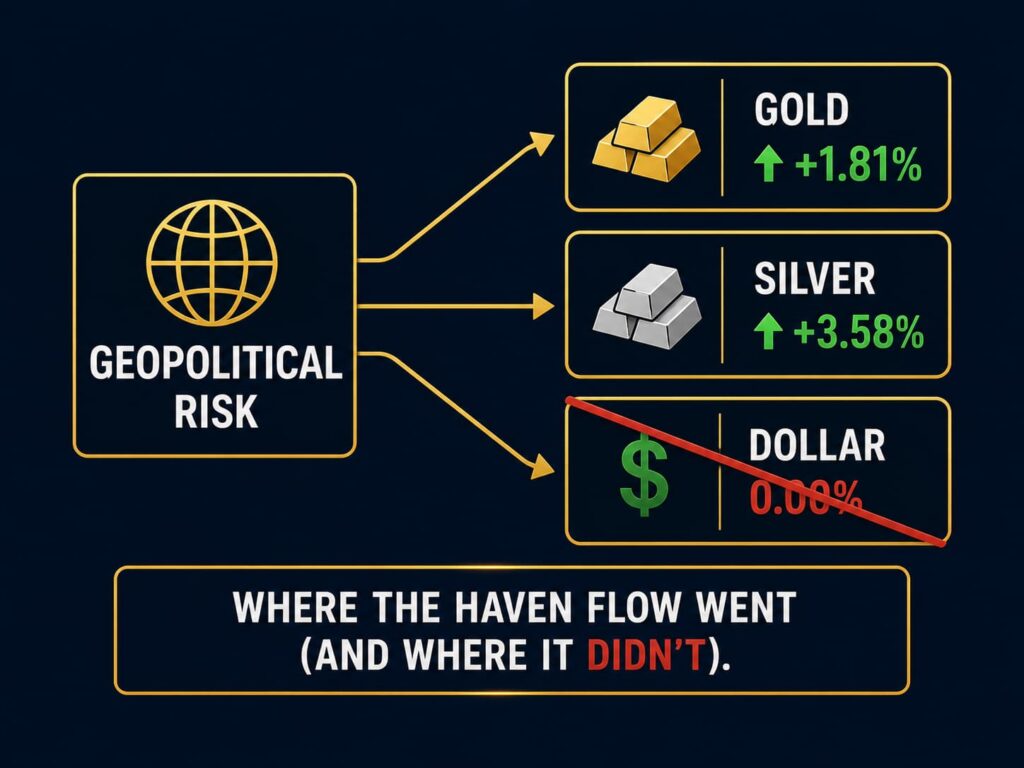

The dollar didn’t move. That’s the story of this friday wrap. Gold ripped almost 2%, the VIX popped nearly 5%, Houthi headlines crossed the wire, and the DXY sat at 100.857, unchanged on the day. The tape said risk-off. The dollar said “not my problem.” That divergence is the entire macro read.

In one sentence: on 3 July 2026 the DXY closed dead flat at 100.857 while gold surged 1.81% to $4,187 and the VIX bid 4.82% — a classic risk-off tape where the dollar refused to play the safe-haven role, telling the desk the marginal buyer of USD is missing at these yields. This friday wrap breaks down why.

For a deeper look at [how the Fed shapes the dollar], this friday wrap recommends understanding the rate spine that held the dollar back.

The Close, in One Glance

The headline is the flatness. The DXY closed 100.857, down a rounded zero on the day, essentially unchanged. That number should not exist on a session where gold added 1.81%, silver 3.58%, and the VIX bid nearly 5%. In a textbook risk-off tape the dollar is the second haven behind Treasuries. Today it wasn’t. This friday wrap treats that as the signal of the session.

Walking the majors against the buck, every G10 pair drifted the dollar’s way against it. EUR/USD sat at 1.1439 (+0.14%). GBP/USD at 1.3350 (+0.08%). USD/JPY the only pair where the dollar held ground, printing 161.348 (-0.06%), and even there the move was noise. USD/CHF at 0.8029 (-0.19%) told the cleaner haven story, capital rotating into francs, not dollars. AUD/USD at 0.6941 (+0.36%) and NZD/USD at 0.5709 (+0.28%) added the risk-currency confirmation, which is odd for a risk-off tape and worth flagging in this friday wrap.

This friday wrap has to reconcile two contradictory tapes. Equities were mixed — S&P 500 at 7,136.50 (+0.40%) closed green while the Nasdaq 100 at 26,696.48 (-0.31%) closed red, a classic defensive rotation inside the index. Add gold up 1.81% and the VIX up 4.82% and the risk-off signature is unambiguous. But the dollar didn’t get the memo. That’s the trade the desk is thinking about.

For more on [trading key levels and structure], this friday wrap covers how to use technicals to time entries.

The Macro Read Behind the Flat Print

Start with what’s on the tape. There was no tier-1 US data scheduled in this window, so the session was driven by positioning, central-bank rhetoric, and headline flow. Absent a data catalyst, the dollar’s price action was pure order flow against a headline backdrop, which makes today more diagnostic than an NFP or CPI day. This friday wrap finds today tells us where the marginal bid actually sits.

The marginal bid did not sit with the dollar. That’s a positioning statement. When the DXY refuses to bid on a day the VIX gaps 5% and gold rips 2%, the interpretation is either (a) dollar longs are already extended and there’s no incremental buyer, or (b) the market is quietly re-pricing the terminal Fed rate lower and dollar carry no longer compensates for the reserve status. Both are the same trade in different clothing. This friday wrap treats that as the key question for the next session.

Cross-reference this against the Federal Reserve’s monetary policy stance and the picture sharpens. The Fed is in an on-hold posture with the market pricing modest cuts into the back half. That’s the differential lens. Every other G10 central bank is either cutting faster (ECB, BoC, BoE guided-dovish) or standing pat (BoJ still normalising, RBA / RBNZ near neutral). The rate differential should support the dollar. It isn’t. Which means something else is offsetting the yield story, and the desk’s read is that geopolitical premium is pushing capital into gold, francs and yen, not dollars. This friday wrap frames that divergence as the session’s central story.

For the official source, the Federal Reserve publishes the monetary policy framework that shapes this rate spine.

The Geopolitical Engine: Houthis, Saudis, and the French Carrier Group

The headline that hit the tape at 20:10 GMT, right at the cash close, was the Houthi statement: “Any further Saudi attack would be met with strikes on Saudi airports and vital interests.” That is an escalation threat aimed at critical infrastructure in the world’s largest crude exporter. The market did not price the full weight of it into today’s close because it landed at the bell, but the hedges that were being layered into the session anticipated exactly this kind of headline. The gold move was ahead of the print, not behind it. This friday wrap reads that as a signal of live premium, not residual carry.

Layer on the French dimension. President Macron confirmed that France has “deployed mine countermeasures assets to the Middle East, including two minehunters,” and stated that the aircraft carrier Charles de Gaulle is “returning to its home port in Toulon” while “mine countermeasures assets and their escort remain deployed and ready to intervene alongside our partners.” The French are pulling the carrier back but leaving the minehunters and their escort in theatre. That is a specific posture: naval mine risk in the shipping lanes is being treated as the primary threat vector, not carrier-strike operations. This friday wrap notes that the geopolitical premium is now structural, not temporary.

What does this mean for markets in one line? The war premium in oil, gold and silver is not a residual carry from earlier in the year. It is a live premium tied to shipping-lane security in the Bab-el-Mandeb and the Strait of Hormuz. Brent settled at $72.12, so crude is not screaming panic. But the metals are pricing that if the Houthis follow through on the Saudi-airport threat, the tape will not unwind gently. That is the risk this friday wrap is watching into next week.

For the official source, Reuters provides the wire coverage of these geopolitical developments.l developments.

The Persian Gulf Power Shift: Why the Strait Is the Real Story

The geopolitical story of the session is not just about a single Houthi threat. It is about a structural shift in the Persian Gulf that most market commentary is missing. As one analysis put it, the U.S.-Iran ceasefire negotiations and the transfer of control of the Strait of Hormuz are painting a “textbook-level macro landscape” .

Although ships can pass freely during the 60-day ceasefire period, the Iranian armed forces have issued a tough warning, requiring all merchant ships to use Iranian-designated routes. More importantly, Omani officials, along with their European and some Gulf state counterparts, have privately acknowledged that a return to pre-war status is impossible. In the future, paying “passage fees” or “service fees” to Iran and Oman for the Strait of Hormuz is becoming an inevitable trend .

This is a structural change that markets have not fully priced. Currently, overall shipping volumes through the strait remain about 70% below pre-war levels. This long-term supply chain disruption and change in sovereign control means that although international oil prices have temporarily fallen due to the ceasefire, the geopolitical risk premium has not dissipated .

For this friday wrap, the geopolitical risk has shifted from “acute panic over outbreak of conflict” to “chronic anxiety over rebuilding order.” The normalization of tolls in the Strait of Hormuz is a sign of the shaking of American maritime hegemony. The resulting structural rise in global shipping costs and long-term inflation expectations will continue to drive safe-haven inflows into the gold market . That is the deeper read of this friday wrap.

Gold, Silver and the Anti-Dollar Bid

Gold closed at $4,187.30, up 1.81% on the session. Silver at $62.815, up 3.58%. The metals had the day. This is where the anti-dollar signal is loudest. When gold rips 2% on a session where the DXY holds flat, the message from real-money flow is that the marginal safe-haven allocation is going into bullion, not into Treasuries or the dollar. This friday wrap treats that as the key signal.

Silver outperforming gold by ~2:1 is a tell of its own. The gold-silver ratio compression on strong days signals the industrial-plus-monetary demand blend, not just haven buying. That’s consistent with the geopolitical driver — silver has an industrial component (solar, electronics) that benefits from supply-chain-risk pricing in a way gold does not.

The $4,200 round is the immediate overhead resistance for gold, and above that the prior week’s high sits as the next liquidity target. Below, $4,150 is the round-number pivot from earlier in the week, and $4,100 is the broader psychological floor.

For more on [gold trading strategies] (path: /guides/the-relationship-between-gold-and-forex), this friday wrap covers how real yields and the dollar drive the metal.

The Dollar and Yields Did Not Confirm

Here is where the session gets interesting for the DXY watchers. On a genuine risk-off day driven by geopolitical escalation, you would expect the dollar to catch a haven bid. DXY closed at 100.857, essentially unchanged. That is a striking non-response.

Why did the dollar not catch? Two reasons the desk is running with in this friday wrap. First, the escalation risk is dollar-adjacent — US treaty allies in the Gulf are the exposure, so the dollar is not a clean haven against the specific shock. Second, EUR/USD closed +0.54% at 1.1439 and GBP/USD closed +0.56% at 1.3354, both catching bids on their own domestic reads. USD/JPY dropped 0.73% to 161.35, the yen doing the genuine haven work.

Yields did nothing visible in the snapshot window. That matters. When gold rallies 1.81% and real yields do not fall, the entire move is a risk-premium move, not a discount-rate move. That is a purer haven signal, and it is why the desk is reading through the flat DXY print rather than concluding “no risk-off happened.”

This friday wrap frames the divergence as the key question for the next session: either gold fades or the dollar breaks lower.

USD/JPY: The Yen Is Trapped at 161

USD/JPY at 161.348 (-0.06%) is the pair that anchors the dollar’s refusal to fall. On a risk-off day the yen should be catching a bid harder than gold. It isn’t. The reason is structural: the Bank of Japan’s terminal rate is still below 1%, the Fed’s is above 4%, and even with cuts priced into the Fed path the differential is enormous. The carry trade is not dead. It’s just paused. This friday wrap reads that pause as the reason the dollar held flat despite the risk-off tape.

The 162 round is the level the desk is watching as the next major liquidity pool above. The intervention risk from the Ministry of Finance clusters in the 162 to 165 zone, and every 20 pips higher the probability of a verbal warning rises. Below, 160 is the round-number support, and below that the June low is the structural pivot for the pair. This friday wrap treats USD/JPY as the anchor that held the dollar from breaking lower.

Japan’s Finance Minister Katayama reiterated that authorities are “ready to act appropriately” in response to excessive currency fluctuations and are “coordinating closely with the US.” This is the intervention threat that keeps USD/JPY capped near 162. For this friday wrap, the intervention risk is the invisible hand that prevents the pair from running higher while the dollar refuses to bid.

The Houthi Headline and the Middle East Premium

The 20:58 GMT Houthi headline is the catalyst that explains half the session’s tape: “Any further Saudi attack would be met with strikes on Saudi airports and vital interests.” That’s a direct threat to Saudi infrastructure, which prices back into oil supply risk, which prices into gold, silver, and the VIX. The chain from headline to price took less than two hours .

The French naval deployment adds another layer. Mine countermeasures assets in the Middle East signal that the shipping lane threat is being taken seriously at the highest levels. The Charles de Gaulle returning to Toulon while the minehunters remain is a specific posture: naval mine risk is the primary threat vector, not carrier-strike operations.

This friday wrap treats the geopolitical premium as live, not residual.

The Sentiment Regime

Desk sentiment engine reads the tape as RISK_OFF, composite score -28. Vol regime ELEVATED. USD bias NEUTRAL. Gold bias BULLISH, composite +28. The gold-versus-DXY divergence is the loudest single signal in the session. Historically, when gold prints +1.8% on a risk-off day and the DXY holds flat, the next 24 to 72 hours tend to see dollar weakness catch up to the anti-dollar signal from bullion. That’s not a forecast, that’s a base rate for this friday wrap.

To ground the mechanism, the index is 57% euro, 14% yen, 12% sterling. So DXY flat while EUR/USD is up 0.14% and USD/JPY down 0.06% and GBP/USD up 0.08% is arithmetically consistent — the euro strength and yen strength offset each other’s dollar-weakening effect. The interesting piece is why the dollar hasn’t broken lower on the composite pressure. The answer, again, is USD/JPY holding 161 by the differential trade .

The Korea Data Footnote

One more headline worth flagging: South Korea’s Q2 exports hit a record $270 billion, with June exports up 59.5% YoY on AI-driven demand. That’s a global growth positive, semiconductor cycle running hot, and reads dollar-neutral to dollar-negative on the margin (KRW strength implies capital rotation into Asian assets, which historically comes at the dollar’s expense). Not a session driver today, but a background flow to note in this friday wrap.

Cross-Asset Impact Dashboard

| GREEN (↑) | RED (↓) |

|---|---|

| Gold $4,187.30 ↑ (+1.81%) | DXY 100.857 ↓ (unchanged, weak on a haven day) |

| Silver $62.815 ↑ (+3.58%) | USD/CHF 0.8029 ↓ (-0.19%) |

| VIX 20.13 ↑ (+4.82%) | USD/JPY 161.348 ↓ (-0.06%, marginal) |

| EUR/USD 1.1439 ↑ (+0.14%) | NDX 26,696 ↓ (-0.31%) |

| GBP/USD 1.3350 ↑ (+0.08%) | DJI 49,246 ↓ (-0.13%) |

| AUD/USD 0.6941 ↑ (+0.36%) | NKY 59,471 ↓ (-0.38%) |

| SPX 7,136.50 ↑ (+0.40%) | DAX 24,059 ↓ (-0.09%) |

| BTC $62,671 ↑ (+1.87%) | FTSE 10,399 ↓ (-0.01%) |

Asset-by-Asset Positioning Read

| Asset | What’s Priced | Direction |

|---|---|---|

| DXY (100.857) | Fed on hold, no marginal buyer at these yields | Neutral, biased soft |

| EUR/USD (1.1439) | Rate-differential compression, ECB near done | Grinding higher |

| USD/JPY (161.348) | Carry trade intact, intervention risk overhead | Pinned in range |

| Gold ($4,187) | Geopolitical premium plus anti-dollar allocation | Bid persistent |

| VIX (20.13) | Elevated vol regime, hedge demand rising | Bid |

What Would Invalidate This View

A good friday wrap always knows what would prove it wrong. The desk runs four invalidation triggers for the current read.

A DXY close above 101.50 would break the recent lower-highs pattern and say the anti-dollar signal from gold was noise. That would invalidate the “dollar refuses to bid” thesis of this wrap and force a re-assessment of the haven flow interpretation.

A gold close back below $4,150 would neutralise the geopolitical premium interpretation and put the metal back in consolidation. This friday wrap would need to re-evaluate whether the gold move was a genuine haven signal or a positioning-driven spike that is now fading.

A VIX close below 18 would flip the regime from ELEVATED back to NORMAL and drain the safe-haven allocation trade of urgency. This friday wrap treats the vol regime as the confirmation of the risk-off tape. A VIX below 18 would suggest the fear was temporary and the geopolitical premium is not structural.

A USD/JPY break above 162 with follow-through would signal the differential trade has more juice than the desk credits and re-rates the dollar composite higher. This friday wrap would need to acknowledge that the carry trade has re-engaged and the dollar is finally catching the bid it refused today.

The desk’s key phrase for the next 24 hours is this: “Watch the divergence, not the levels.” The single most important tell in the next session is whether gold and the DXY re-converge — either the metal gives back and the dollar was right to hold, or the dollar breaks lower and the metal was right to rip. Both cannot be true beyond another 24-48 hours. This friday wrap framework will read the same way tomorrow — the levels shift, the divergence signal doesn’t.

Final Takeaway

The friday wrap for 3 July 2026 hinges on a single anomaly: the DXY refused to bid on a risk-off day, and gold ripped almost 2% into the vacuum. That divergence is either a warning shot for dollar longs or a headline-driven spike that fades. The next session decides. What the desk knows is that a flat DXY on a VIX-bid day means the marginal buyer of dollars is absent at these levels. Absent buyers create the conditions for asymmetric moves lower, not higher.

“When the dollar refuses to bid on a haven day, the tape is telling you something the yield curve isn’t. Listen to the tape, then check the yields, in that order.”

Disclaimer

This article is for educational and informational purposes only. It does not constitute financial advice, trading recommendations, or an offer to buy or sell any asset. Trading forex, commodities, indices, cryptocurrencies, and futures carries significant risk and may not be suitable for all investors. You can lose more than your initial deposit. Past performance does not guarantee future results. Always read full terms, contract specifications, and risk disclosures before trading. Do your own research. Consult a licensed financial advisor if you need professional investment advice.