One number runs this cpi week and the two after it. US inflation lands Tuesday, and it decides whether a July rate hike goes from a tail risk to a live debate. Everything else – PPI, the Fed Chair’s testimony, the Bank of Canada and UK growth – is read through that lens.

This cpi week is the fulcrum for the whole run into the Federal Reserve decision on the 28th and 29th of July. Get the read on inflation right and you have the map for the dollar, gold, stocks and bonds for a fortnight. The desk has said it all week and we will say it again plainly: this is a cpi week , and CPI this month is not just another data point.

The Fed has stopped pricing cuts and started leaning higher for longer, with the Chair keeping the door open. The market has been comfortable that any further hike is a Q4 story. This cpi week can challenge that. If inflation proves sticky, the question the desk is watching is simple and loud: does a hike come as early as July, and does the market start pricing it above a coin flip by Friday.

For a deeper look at [how the Fed shapes the dollar], this cpi week guide recommends understanding the rate spine that drives the greenback.

The High-Impact Calendar for CPI Week

| When (BST) | Event | Why It Matters |

|---|---|---|

| Tue 14, 13:30 ★ | US CPI (June) | The centerpiece. Core is the tell. Sets the tone into the FOMC. |

| Wed 15, 13:30 | US PPI (June) | The pipeline read on inflation. Confirms or fades the CPI signal. |

| Wed 15, 14:45 | Bank of Canada | Rate decision and Monetary Policy Report. Currently 2.25%. |

| Midweek | Fed Chair Warsh testimony | Semi-annual monetary policy report to the House Financial Services Committee. Listen for the July tone. |

| Thu 16, 07:00 | UK GDP (monthly) | The growth pulse for sterling and the BoE path. |

This cpi week calendar is the roadmap. Every event feeds into the same question: does inflation stay sticky enough to force a July hike? The desk reads this cpi week through that lens.

US CPI: Why Core Is the Number That Moves the Board

Headline CPI grabs the news. Core CPI moves the market. Core strips out food and energy, and this cycle it also strips out the noise of a volatile oil price that has swung hard on the Middle East. That is the whole point. The Fed cannot set policy off a petrol price that jumps ten percent on a headline and gives it back a week later. It steers by the underlying trend, and the underlying trend is core.

So the desk’s eyes go straight past the headline to core, month on month, and to the trend underneath it. Is core cooling, stalling, or reaccelerating? A stall or a reacceleration in core is what puts a July hike on the table, because it says the last mile of inflation is not coming down, and a Fed that is already leaning hawkish has its excuse.

The desk’s lean into the print. We lean toward stickier inflation still showing up. If core comes in firm, and PPI backs it up on Wednesday, and Warsh keeps a hawkish tone in his testimony, the pricing for a July hike can push above fifty percent by the end of the week. That is the scenario the desk is most alert to, and it is the one the market is least positioned for. This cpi week will test that positioning.

For the official source, the US Bureau of Labor Statistics publishes the CPI data that defines this cpi week.

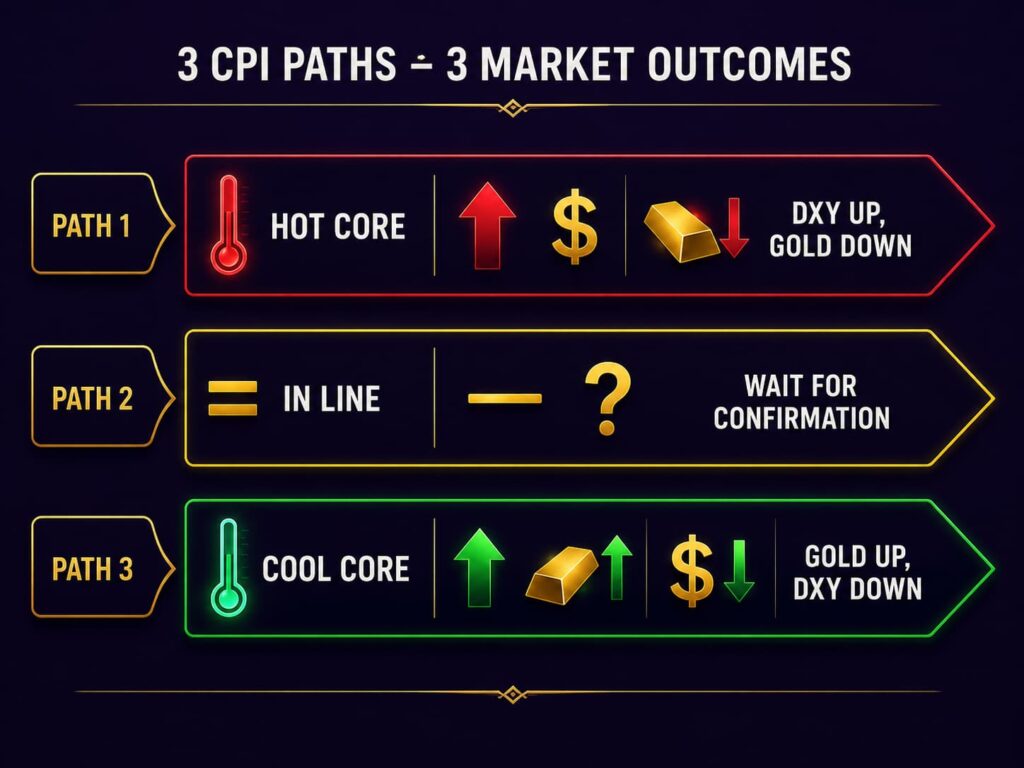

Three Paths Through CPI Week, and What Each Does to the Board

1. Hot print, core firm or above

The scenario the desk weights most. Sticky core, backed by PPI, revives the July hike debate. Real yields spike, the dollar follows, gold comes under heavy selling pressure, and stocks sell off as the discount rate rises. A hot print plus a hawkish Warsh is the cleanest, most dangerous combination for risk this cpi week.

2. In line

The market exhales, but only for a session. In line keeps the Fed exactly where it is – higher for longer – and hands the microphone to Warsh and PPI to break the tie. Expect a muted first move, then positioning and the details – core services, shelter – decide the direction. Do not chase the first candle. This cpi week requires patience.

3. Cool print, core soft

The relief trade. A soft core takes the July hike off the table and lets the pressure valve open: gold and stocks bounce, the dollar and yields ease. The desk’s caution: in a higher for longer regime the relief move is often sharp but shorter lived, unless it is a clean break in the trend. Respect the direction the yields are setting. This cpi week could flip quickly.

PPI: The Confirmation on Wednesday

Producer prices are the pipeline. They tell you what is coming down the line to the consumer. If CPI runs hot on Tuesday and PPI confirms it on Wednesday, the inflation story hardens and the July hike pricing has real fuel. If PPI fades a hot CPI, the market gets an off-ramp. The desk reads the two together, not in isolation. This cpi week is really a CPI-PPI week.

Warsh Testifies, and the Tone Is the Trade

The Fed Chair delivers the semi-annual monetary policy report to the House Financial Services Committee this cpi week. This is not a data release, it is a signal. The desk is listening for one thing: how open is Warsh to acting sooner rather than later. A Chair who sounds relaxed about sticky inflation calms the July debate. A Chair who sounds impatient, right after a hot CPI, is the market’s cue to price the hike. Tone, not text, is the trade.

For the official source, the Federal Reserve publishes the monetary policy framework that shapes this cpi week.

How the Desk Holds Each Market Through CPI Week

Dollar (DXY). Structurally still leans up on higher for longer and elevated real yields. A hot CPI is the accelerant. The desk respects the trend and lets the reaction confirm.

Gold (XAU/USD). The most exposed to a hot print. Real yields have been overwhelming the haven bid, and a firm core plus a spike in yields is heavy for gold. The one override remains a fresh geopolitical shock.

Stocks (S&P, Nasdaq). Vulnerable to a higher discount rate. A hot CPI that lifts yields pressures the multiple. A cool print is the relief.

Yields (US 2y, 10y). The lead indicator all week. If the front end pushes higher on hike pricing, believe the dollar move. If yields diverge, be careful.

GBP/USD: What Actually Moves Cable

GBP/USD, the pair traders call cable, is at heart a rate differential story between the Bank of England and the Federal Reserve. The pound tends to firm against the dollar when the market expects the Bank of England to hold rates higher relative to the Fed, and to soften when the Fed is expected to stay tighter for longer. Each UK or US inflation print, jobs report and central bank meeting reprices that gap, which is why cable can move sharply on data from either side of the Atlantic.

Two other forces layer on top. The first is UK specific risk: politics, fiscal headlines and growth surprises can move the pound on their own, independent of the dollar. The second is the broad dollar, since in a risk off episode the dollar’s haven status can override the UK story entirely and drag cable lower even when nothing has changed at home. The desk reads GBP/USD as the Bank of England path minus the Fed path, adjusted for UK risk and wherever global risk appetite sits.

Cable respects round numbers and prior swing levels closely. The structure stays constructive while price holds above its nearest defended support and the run of higher lows is intact, and turns cautious when a support that held several times finally gives way on a closing basis.

EUR/USD: The Rate Differential Trade

EUR/USD is the world’s most traded pair and at heart it is a rate differential story. The euro tends to firm against the dollar when the market expects the European Central Bank to hold rates higher relative to the Federal Reserve, and it tends to soften when the Fed is expected to stay tighter for longer. That is why the pair reacts so sharply to inflation prints and central bank meetings on both sides of the Atlantic: each one reprices the gap between the two policy paths.

Relative growth and risk appetite layer on top. A stronger euro area growth surprise narrows the gap the market expects and supports the euro. Broad dollar strength in a risk off episode can override the rate story for a while, since the dollar is the world’s haven. The desk reads EUR/USD as the ECB path minus the Fed path, adjusted for who is growing and where global risk appetite sits.

EUR/USD respects clean horizontal structure and the big round figures. The near term bias stays constructive for the euro while price holds its nearest defended support and prints higher lows; it turns heavy when a support that held repeatedly breaks on a closing basis.

For more on [trading major currency pairs], this guide covers how cpi week data affects FX.

USD/JPY: The Cleanest Yield Gap Trade

USD/JPY is the cleanest yield gap trade in the major currencies. The pair tracks the difference between US and Japanese long term yields: when US yields sit far above Japanese yields, capital flows into the higher yielder and the dollar tends to rise against the yen. As the Bank of Japan normalises policy and that gap narrows, the structural tailwind for the pair fades. This is also the engine of the yen carry trade, where investors borrow cheaply in yen to buy higher yielding assets, a flow that can unwind violently when volatility spikes.

The second force is intervention. When the yen weakens too far too fast, Japan’s Ministry of Finance can step in to buy yen and sell dollars, which produces sharp, fast reversals near well watched round levels. That is why the upper end of the range carries a different kind of risk than a normal trend: the desk treats the big figures up there as intervention zones, not just chart levels.

USD/JPY trends hard on the yield gap, then snaps on intervention and carry unwinds. The near term bias stays firm for the dollar while price holds its nearest defended support and the yield gap is wide; it turns two sided fast near the intervention zones and whenever risk volatility jumps.

The Gold Forecast for CPI Week

What sets the price: gold is priced off three forces, real US yields (the 10 year Treasury yield after inflation), the US dollar, and steady central bank demand. Everything else matters only through those three. This cpi week , the first two forces are the ones that will move gold the most. What is supportive: falling real yields and a softer dollar lower the cost of holding a non yielding asset, so gold tends to firm. Rising real yields and a firmer dollar are the headwind. This cpi week will test which force wins.

The haven bid: a fear spike can lift gold regardless of yields, but it fades fast unless it also pulls the rate path lower. The desk treats a haven pop as durable only when it also shows up in yields and the dollar. This cpi week , the haven bid is secondary to the inflation read.

Real yields are the deepest driver, because they set the true opportunity cost of holding metal that pays nothing. A real yield is the nominal Treasury yield minus expected inflation, and it moves on two things: where the market thinks the Fed is heading, and where it thinks inflation is going. When the market prices Fed cuts and cooling inflation, real yields fall and gold tends to grind higher. When it prices a higher for longer Fed or sticky inflation, real yields rise and gold struggles. This cpi week will decide which direction real yields take.

The third channel is fear. Gold is a haven, so in genuine risk off episodes, a banking scare, a war escalation, a sharp equity sell off, capital rotates into it and the price can spike regardless of yields and the dollar. The catch is that haven bids fade fast when the panic does. A geopolitical flare that does not change the rate path tends to give back its gains within days, while a shock that forces the Fed to ease can leave a lasting mark because it pulls real yields down too. The desk treats a haven spike as durable only when it also shows up in the yield and dollar channels.

The Bank of Canada – Likely the Quiet One

The Bank of Canada announces on Wednesday with its Monetary Policy Report, from a policy rate of 2.25 percent. The desk’s read is that this is most likely a hold and could be close to a non-event for global markets, with the interest in the tone and the growth and inflation projections rather than the rate itself. Worth watching for the Canadian dollar and as a read on how a peer central bank is framing the same inflation problem, but it is not the week’s driver.

For this cpi week , the BoC is a secondary read. The primary focus remains US inflation and the Fed path. However, the BoC’s framing of energy-driven inflation and its growth projections will be read through the same lens as the US data. If the BoC sounds more hawkish than expected, it could add a marginal bid to the loonie. If it sounds dovish, it could weigh on CAD.

The Canadian jobs print earlier in the week already set the stage. The BoC’s policy statement will confirm or challenge that read. But for this cpi week , the BoC is a footnote to the main event: US inflation and the July hike debate. The desk will monitor it, but it will not trade it as a primary catalyst.

The Tails, Both Sides

The desk is not in the prediction business, it is in the preparation business. The upside tail for risk is a genuinely cool core that breaks the trend and reopens the cut debate. The downside tail is the one we weight more heavily this cpi week : sticky core, confirmed by PPI, endorsed by a hawkish Warsh, that drags July hike odds above fifty percent, spikes real yields, bids the dollar, and sends gold and stocks lower together. Size for both. Trade the reaction, not the headline.

Bottom Line

This cpi week is the fulcrum for the entire July FOMC cycle. Core is the tell. PPI confirms or fades. Warsh’s testimony sets the tone. The dollar, gold, and equities all hinge on whether inflation proves sticky or starts to cool.

The desk leans toward stickier inflation still showing up. If core comes in firm, the July hike debate becomes live. If it cools, the relief trade is sharp but likely short-lived.

Watch core. Watch Warsh. Watch the reaction, not the headline. This cpi week decides the next fortnight.

Disclaimer

This article is for educational and informational purposes only. It does not constitute financial advice, trading recommendations, or an offer to buy or sell any asset. Trading forex, commodities, indices, cryptocurrencies, and futures carries significant risk and may not be suitable for all investors. You can lose more than your initial deposit. Past performance does not guarantee future results. Always read full terms, contract specifications, and risk disclosures before trading. Do your own research. Consult a licensed financial advisor if you need professional investment advice.