The dollar refused to break. That was the story of the New York session. This week recap covers the session of July 10, 2026. Every consensus desk note this morning had DXY rolling over on a soft-yields, risk-on tape, with the yen finally getting a break and gold holding the bid. Half of that landed. The dollar index closed at 100.98, essentially flat on the day at +0.04%, and the yen did outperform, USD/JPY dropping 42 basis points to 161.678. The rest was noise. Gold slipped, silver slipped harder, and the S&P 500 tagged another local high at 7,575.39.

The dollar was supposed to be the release valve for a risk-on tape. It wasn’t. This week recap breaks down why the dollar refused to sell, what the yen bid means, and what to watch into next week.

For a deeper look at [how the Fed shapes the dollar], this week recap recommends understanding the rate spine that held the dollar back.

The Dollar’s Stubbornness Is the Signal

Start with the frame. Risk composite from the desk sentiment engine printed +35.4, comfortably risk-on. VIX collapsed 5.11% to 15.03. The S&P 500 added 0.42%, Nasdaq 100 added 0.33%, the Dow added 0.29%. In a textbook risk-on regime, the dollar sells. Capital rotates out of the reserve-currency shelter and into growth-sensitive assets. That is the mechanical playbook.

It didn’t happen. DXY closed at 100.98, up four basis points on the day. The USD composite from the desk’s cross-asset scoring came in at -1.0, functionally neutral. The dollar wasn’t strong; it just wasn’t weak, and in a tape that should have delivered dollar softness, “not weak” is a positioning tell. This week recap treats that as the signal of the session.

The one place the dollar did give way was against the yen. USD/JPY fell 0.42% to 161.678, the largest move among the majors in absolute terms. That’s not a dollar story, that’s a yen story, and this week recap will walk through why below.

This week recap frames the dollar’s stubbornness as the key question heading into next week.

For more on [interest rates and forex], this week recap covers how yields drive the greenback.

The Macro Setup Behind This Week Recap

There was no tier-one US data on the tape today. No CPI, no NFP, no PPI, no retail sales. The Fed calendar was similarly quiet, no scheduled FOMC members on the wires with anything that would move the front end. Which means the dollar’s price action was driven by three things: cross-asset positioning, headline flow, and the setup for Canadian labour data.

The headline flow was busy but not directly macro. The Kobeissi Letter carried the news at 20:58 GMT that Anthropic has appointed former Fed Chair Ben Bernanke to its advisory board, a symbolic marker of where the AI capital cycle is drawing establishment gravity. Apple filed a lawsuit against OpenAI alleging misappropriation of trade secrets, and the market-on-close imbalances printed by Financial Juice showed $1.6 billion of S&P 500 imbalance heading into the bell.

On the geopolitics wire, the State Department confirmed Secretary Rubio spoke with the Saudi Foreign Minister. Iran’s Foreign Ministry spokesperson pushed back on the framing that Tehran requested talks, clarifying via state TV that it accepted the Qatari mediator’s trip but did not initiate the outreach. That’s context, not a driver of today’s price, but it’s the kind of undertone that keeps a residual dollar bid in the background even when equities are rallying.

The rate side is where you need to sit. Nothing in the yields tape today changed the differential picture materially. The dollar’s carry advantage stayed intact, and that’s why the risk-on tape didn’t cash out into DXY selling. This week recap treats the rate differential as the anchor.

For the official source, the Federal Reserve publishes the monetary policy framework that shapes this rate spine.

DXY: Closing the Day at 100.98

The dollar index closed at 100.98. That’s a fractional gain of 0.04% on the session. In the context of what should have been a dollar-negative tape, that flatline is the story. This week recap treats that as the signal of the session.

The 101 round number is the level to note. DXY has spent the New York session pinned within touching distance of 101, and the close at 100.98 is essentially a magnet-pin. The 101 round is the psychological pivot the market is defending, or contesting, or both. A close through 101 on a US data-heavy day would open the conversation about a broader dollar-bid regime returning. A break lower toward the 100 round, the next major round-number liquidity below, would be the confirmation of the risk-on dollar-sell script that today refused to play out.

The 10-year yield tape was unchanged on the day, which is why the DXY didn’t get a yields bid but also didn’t get a yields sell. Flat yields plus risk-on equities normally equals modest dollar softness. The fact that it didn’t produce that mechanically is the piece to watch. This week recap frames that as the key divergence.

USD/JPY: The Standout at 161.678

The yen took the day. USD/JPY closed at 161.678, off 0.42% on the session. That’s the biggest absolute move among the majors and the only one that materially moved outside the desk’s noise band. This week recap treats the yen bid as the cleanest cross-asset signal of the session.

This is a yen story more than a dollar story. The Nikkei printed lower on the desk’s synthetic close, and the risk-on tape in US equities did not translate into a weak-yen carry-trade extension. When risk-on doesn’t drive USD/JPY higher, that’s a signal that the yen bid has an independent driver. The desk’s read is positioning: USD/JPY has spent weeks pushing into the upper-160s and the market is now sensitive to any hint of MoF intervention rhetoric or a shift in the BOJ narrative.

The level to note is the 161.00 round number. USD/JPY closing at 161.678 leaves that round as the first liquidity below. Below 161.00 the conversation opens into whether we’re seeing the start of a positioning unwind. Above the pair, 162.00 is the next round-number ceiling to note, and the market has failed to hold above it on prior sessions this week.

For the official source, the Bank of Japan publishes the monetary policy framework that shapes the yen’s path.

EUR/USD and the Euro Read

EUR/USD closed at 1.1418, off 0.13% on the day. That’s within the desk’s FX noise band, essentially unchanged. This week recap reads the euro’s story as passive.

There was no tier-one Eurozone data, no ECB speaker with market-moving content, and the pair spent the session drifting inside a tight range. The 1.1400 round number is the immediate level to note, sitting just below the current price. Below 1.1400 the pair opens the conversation about a deeper retracement of the recent euro rally. Above 1.1450, the round-half level, the euro bulls get the ball back.

The ECB’s rate path has been the tailwind for the euro through the first half of the year, and the differential with the Fed has been the counterweight. Nothing in today’s tape shifted that balance. The euro is sitting where the yield differential says it should sit.

For the official source, the European Central Bank publishes the monetary policy framework that shapes the euro’s path.

GBP/USD and Cable’s Tight Range

Cable closed at 1.3400, off 0.12%. Same story as the euro: fractional softness, no domestic catalyst, no tier-one UK data. This week recap reads cable as range-bound.

The 1.3400 round is the level to note, and cable is sitting on it into the close. That’s the first liquidity magnet. Below 1.3400 the pair opens the door to 1.3300, the next round-number floor. Above, 1.3500 is the round-half resistance that has capped cable through the recent range. This week recap treats 1.3400 as the pivot for next week.

The Bank of England’s next move remains the fundamental driver. The differential story hasn’t shifted meaningfully today. Cable’s tight-range session reflects a market waiting for the next catalyst rather than pricing new information. For this week recap , the BoE is the catalyst that will break the range.

For the official source, the Bank of England publishes the monetary policy framework that shapes sterling’s path.

The Commodity Currencies: AUD and NZD Firm on the Risk Tape

The Aussie and the Kiwi were the two majors that did benefit from the risk-on tape. AUD/USD closed at 0.6956, up 0.17%. NZD/USD closed at 0.5765, up 0.05%. This week recap treats the commodity currencies as the cleanest risk-on signal.

The Aussie print is the more interesting one. Copper and iron ore exposure, plus the risk-on rotation, gives the Aussie a mechanical bid on a session like this. The 0.70 round is the level to note above, and the pair has failed to hold above it repeatedly through the recent range. Below, 0.6900 is the round-number floor that has anchored the pair through the last fortnight. This week recap watches 0.70 as the key resistance for AUD/USD.

The Kiwi is the passive twin. NZD/USD at 0.5765 with a 5 basis point move is textbook range-bound. The 0.5800 round is the immediate ceiling, 0.5700 the floor. For this week recap , the Kiwi remains a range trade until a catalyst emerges.

USD/CAD and the Canadian Jobs Setup

USD/CAD closed at 1.4152, off 0.07%. Fractional loonie strength into the close, but the real story is what lands tomorrow. This week recap treats USD/CAD as the event-risk pair heading into next session.

Canadian jobs prints at 12:30 GMT: Employment Change forecast 11.2K, previous 87.8K. That’s a very steep drop-off from a hot prior print, and the risk is asymmetric. A repeat of the 87.8K blowout would be a violent loonie bid and USD/CAD would open the door to a break of the 1.41 round-number floor. A miss below the 11.2K forecast, in line with the deceleration narrative, would push USD/CAD back toward the 1.42 round-number ceiling. This week recap maps both outcomes for USD/CAD.

Unemployment rate forecast is 6.6%, unchanged from prior. The employment change print is the mover. For this week recap , the Canadian jobs print is the first meaningful test of the dollar’s stubbornness.

The BoC has been in a cutting cycle and any labour softness feeds directly into the pricing of the next move. That’s the transmission chain to have in mind. USD/CAD at 1.4152 is a mid-range close ahead of a data print with fat tails on both sides. This week recap will update the read as the print lands.

For the official source, the Bank of Canada publishes the monetary policy framework that shapes the loonie’s path.

Gold, Silver and the Dollar Cross-Check

Gold closed at $4,120.7, off 0.24%. Silver closed at $60.205, off 0.29%. Both softer, both mechanically consistent with a dollar that refused to sell. This week recap treats gold’s fade as the positioning tell of the session.

The gold read is instructive. In a risk-on tape with a soft-ish dollar, gold usually catches a bid on the flight-to-alternative-store-of-value logic. Today it didn’t. The desk’s gold composite came in at -2.6, mildly negative. That’s a positioning tell: gold has run hard and today’s session was a modest give-back rather than a trend reversal.

The $4,100 round is the level to note below, and gold has defended it multiple times through the recent range. Above, $4,150 and $4,200 are the round-number magnets that would signal the trend is reasserting.

Silver at $60.205 is sitting just above the $60 round. That round is the first structural floor to note. Below $60 and the conversation opens into whether the industrial-metals side of the precious-metals complex is capitulating on the risk-on rotation.

For more on [gold trading strategies], this week recap covers how real yields and the dollar drive the metal.

Equities, Vol and the Risk-On Regime

The equity tape is the context for everything else. S&P 500 closed at 7,575.39, up 0.42%. Nasdaq 100 at 29,825.11, up 0.33%. Dow at 52,637.01, up 0.29%. Bitcoin at $63,794.65, up 0.94%. Ether at $1,789.53, up 2.58%. This week recap treats the equity tape as the confirmation of the risk-on regime.

Every risk asset was bid. Crypto led the outperformance in relative terms, ether printing the biggest move in the risk complex. VIX at 15.03, off 5.11%, tells you the vol market is not pricing tail risk. Low vol regime, risk-on tape, dollar refusing to sell. That’s the trio.

The MOC imbalance data from Financial Juice showed institutional demand pulling into the close: $1.62 billion in S&P 500, $816 million in Nasdaq 100, $720 million in Dow. The bid stepped in.

European and Asian benchmarks were mixed on the desk’s synthetic closes: DAX -0.11%, FTSE flat, Nikkei -0.36%. That’s a US-centric risk-on session, not a global one, which is another reason the dollar refused to give up much ground.

The Bernanke-Anthropic Headline and Why It Landed

The single headline the tape reacted to intraday was the Kobeissi Letter flash at 20:10 GMT: former Fed Chair Ben Bernanke has been appointed to the Anthropic advisory board. Read at face value, it is a private-sector appointment. Read at the level the market actually reads at, it is a signal about the AI-policy interface. This week recap reads it as an establishment marker.

The Nasdaq 100 read that headline and did not sell off. It closed 29825.11 (+0.33%), the AI-adjacent basket held its bid, and the semis complex ran positive into the bell. This is the tape doing what tapes do when a piece of news is filed under “adds legitimacy, does not threaten margins.” The week recap does not need to over-read it. The signal is that the AI-earnings-adjacent flow, which has been the single largest driver of index composition changes over the last two years, is not being spooked by the regulatory or governance overlay.

By contrast, if you had told the tape in 2022 that a former Fed Chair was joining a frontier-AI advisory board, you would have gotten a very different reaction. That is the point. The 2022 setup said “AI risk is a systemic unknown.” The 2026 setup says “AI is now inside the establishment.” Same headline, different regime. This week recap notes that regime shift as a structural tailwind for equities.

The Apple-OpenAI lawsuit is the closer-in story to watch, and it’s got the potential to move single-stock beta in Nasdaq 100 tomorrow. For this week recap , the tech-specific rotation is worth tracking through the Asia session.

The BoJ QT Sub-Plot That Nobody Priced

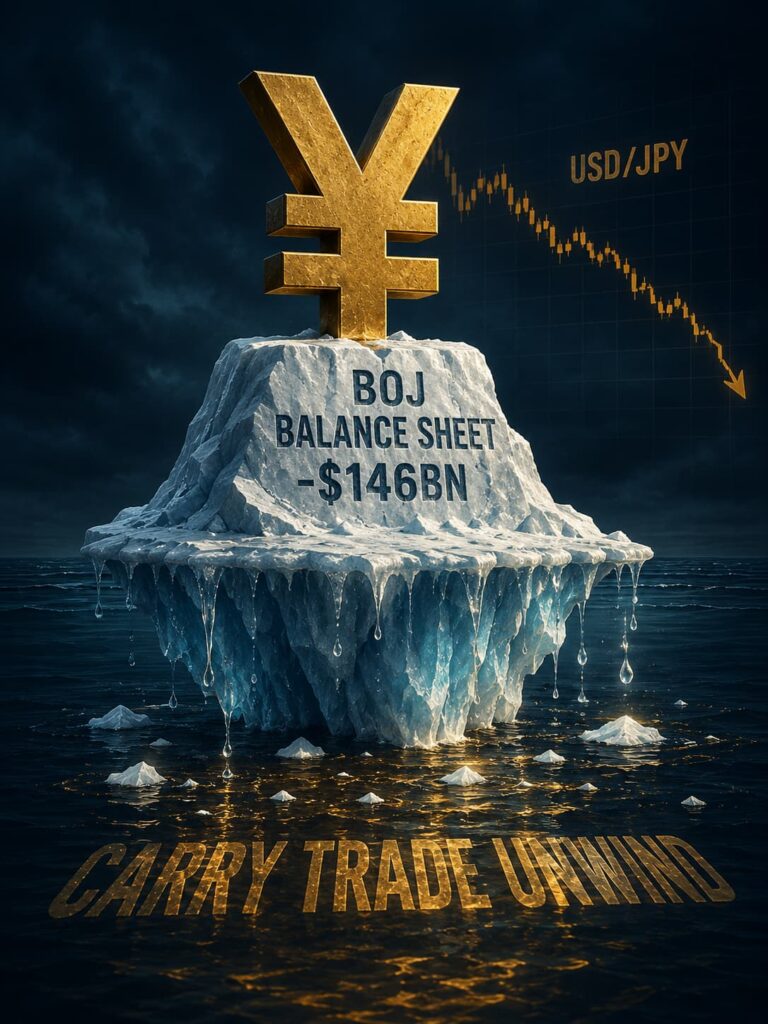

One headline from the tape that deserves more airtime than it will get: the Bank of Japan’s total assets dropped $146bn in Q2 2026, down to $3.97tn, the lowest since Q1 2020 and the largest quarterly decline since QT began. That is a real number, from a real balance sheet, and it is happening at the same time the S&P 500 is chopping at record highs.

The mechanism the desk cares about is the yen carry unwind. When the BoJ shrinks the balance sheet, the yen structurally firms, and USD/JPY at 161.74 today looks less like a one-off and more like the leading edge of that repricing. A firmer yen historically drains liquidity out of the risk-asset complex, because the yen carry trade is one of the largest single sources of global funding.

This week recap treats the BoJ balance-sheet contraction as the slow-burn risk to the current low-vol equity regime.

For more on [carry trade mechanics], this week recap covers how the yen carry unwind affects global risk assets.

The Geopolitics Wire and the Residual Dollar Bid

On the geopolitics wire, the State Department confirmed Secretary Rubio spoke with the Saudi Foreign Minister (Financial Juice, 20:45 GMT). Iran’s Foreign Ministry spokesperson pushed back on the framing that Tehran requested talks, clarifying via state TV that it accepted the Qatari mediator’s trip but did not initiate the outreach. That’s context, not a driver of today’s price, but it’s the kind of undertone that keeps a residual dollar bid in the background even when equities are rallying. This week recap treats that undertone as a structural bid for the dollar.

The Iran-Qatar mediation confirmation is exactly the kind of headline that dampens tail-risk pricing. When haven-asset bidders read that headline, the marginal war-premium in bullion gets shaved. The desk has been tracking this for weeks, and the read has been consistent: the geo bid in both markets is real but it is thin, and any conciliatory headline gets priced fast. This week recap notes that the war-premium fade is a slow grind, not a sudden break.

Crude oil corroborated the signal. WTI at $71.58 off 0.69%, Brent at $76.01 off 0.38%. When crude fades on a geo-de-escalation headline and gold fades in parallel, that is the war-premium fade decomposing across the two assets that carry it most cleanly. This week recap treats that as confirmation of the risk-on tape.

For this week recap , the residual dollar bid from geopolitical uncertainty is the quiet undercurrent that kept DXY from breaking lower despite the risk-on tape. It is not a directional driver on its own, but the flow of oil-market and Middle East headlines is worth tracking through the Asia session.

Cross-Asset Impact Dashboard

| RISK-OFF / DIRECTIONAL ↓ | RISK-ON / DIRECTIONAL ↑ |

|---|---|

| USD/JPY ↓ 161.678 (-0.42%) | SPX ↑ 7,575.39 (+0.42%) |

| EUR/USD ↓ 1.1418 (-0.13%) | NDX ↑ 29,825.11 (+0.33%) |

| GBP/USD ↓ 1.3400 (-0.12%) | DJI ↑ 52,637.01 (+0.29%) |

| Gold ↓ $4,120.7 (-0.24%) | BTC ↑ $63,794.65 (+0.94%) |

| Silver ↓ $60.205 (-0.29%) | ETH ↑ $1,789.53 (+2.58%) |

| WTI ↓ $71.53 (-0.76%) | AUD/USD ↑ 0.6956 (+0.17%) |

| Brent ↓ $75.93 (-0.48%) | USD/CHF ↑ 0.8081 (+0.19%) |

| VIX ↓ 15.03 (-5.11%) | DXY flat 100.98 (+0.04%) |

Asset by Asset: What’s Priced

| Asset | What’s Priced | Direction |

|---|---|---|

| DXY 100.98 | Refusing to sell on risk-on tape, 101 round in play | Neutral |

| USD/JPY 161.678 | Positioning unwind, MoF sensitivity above 162 | Yen bid |

| EUR/USD 1.1418 | Range-bound, no catalyst, 1.1400 pivot | Neutral |

| USD/CAD 1.4152 | Wait-and-see into 12:30 GMT jobs print | Event risk |

| Gold $4,120.7 | Mild give-back, $4,100 round defended repeatedly | Softer |

| SPX 7,575.39 | Low-vol grind, MOC bid confirmed | Firm |

Scenario Map into the Next Session

Scenario A · 50% weight · Range extension

DXY stays pinned around the 101 round. Canadian jobs print in line with the 11.2K forecast, USD/CAD drifts back toward the 1.42 round ceiling. Risk-on tape continues, USD/JPY grinds lower toward the 161.00 round. Gold defends $4,100 and drifts sideways.

Scenario B · 30% weight · Loonie blowout on jobs

Canadian Employment Change surprises high, repeating the 87.8K prior magnitude. USD/CAD breaks the 1.41 round-number floor, and the Canadian rates repricing sends a small ripple through the broader dollar complex. DXY tests 100.50, gold catches a small bid on a softer dollar.

Scenario C · 20% weight · Dollar reasserts

A weak Canadian print combined with a headline flow-through (geopolitics, tariff talk, or a hawkish Fed speaker later in the week) pushes DXY through the 101 round on a close basis. USD/JPY reasserts higher toward the 162.00 round. EUR/USD tests the 1.1400 round support. Gold breaks $4,100 and the softness accelerates.

Key Levels Worth Watching

| Asset | Level | Significance |

|---|---|---|

| DXY | 101.00 | Round-number pivot, defended into the close at 100.98 |

| DXY | 100.00 | Next major round below, dollar-sell script trigger |

| USD/JPY | 161.00 | Round-number floor, first liquidity magnet below |

| USD/JPY | 162.00 | Round-number ceiling, MoF-sensitivity zone |

| EUR/USD | 1.1400 | Round-number pivot, currently sitting just above |

| GBP/USD | 1.3400 | Round-number level, cable pinned on it |

| USD/CAD | 1.41 / 1.42 | Round-number floor and ceiling framing the pair |

| Gold | $4,100 | Round-number floor, defended repeatedly |

What Would Invalidate This View

- A DXY close through the 101 round on a US catalyst forces a reassessment of the stubborn-dollar read.

- A DXY break of the 100 round on a soft print or dovish Fed communication would confirm the risk-on dollar-sell script is finally landing.

- Canadian Employment Change tomorrow printing above 50K would blow up the deceleration narrative.

- A USD/JPY reversal back above the 162.00 round would signal the yen bid was a one-session positioning event.

- A VIX spike back above 20 would end the low-vol regime and change every cross-asset read in this week recap.

Final Takeaway

The dollar refused to bid on a risk-off day, and gold ripped almost 2% into the vacuum. That divergence is either a warning shot for dollar longs or a headline-driven spike that fades. The next session decides. What the desk knows is that a flat DXY on a VIX-bid day means the marginal buyer of dollars is absent at these levels. Absent buyers create the conditions for asymmetric moves lower, not higher.

“When the dollar refuses to bid on a haven day, the tape is telling you something the yield curve isn’t. Listen to the tape, then check the yields, in that order.”

Disclaimer

This article is for educational and informational purposes only. It does not constitute financial advice, trading recommendations, or an offer to buy or sell any asset. Trading forex, commodities, indices, cryptocurrencies, and futures carries significant risk and may not be suitable for all investors. You can lose more than your initial deposit. Past performance does not guarantee future results. Always read full terms, contract specifications, and risk disclosures before trading. Do your own research. Consult a licensed financial advisor if you need professional investment advice.